Forward Looking Market Observations – Economic Cycles and Geopolitical Issues – The 7 Year Pattern, Then and Now

by Leland Lehrman

by Leland Lehrman

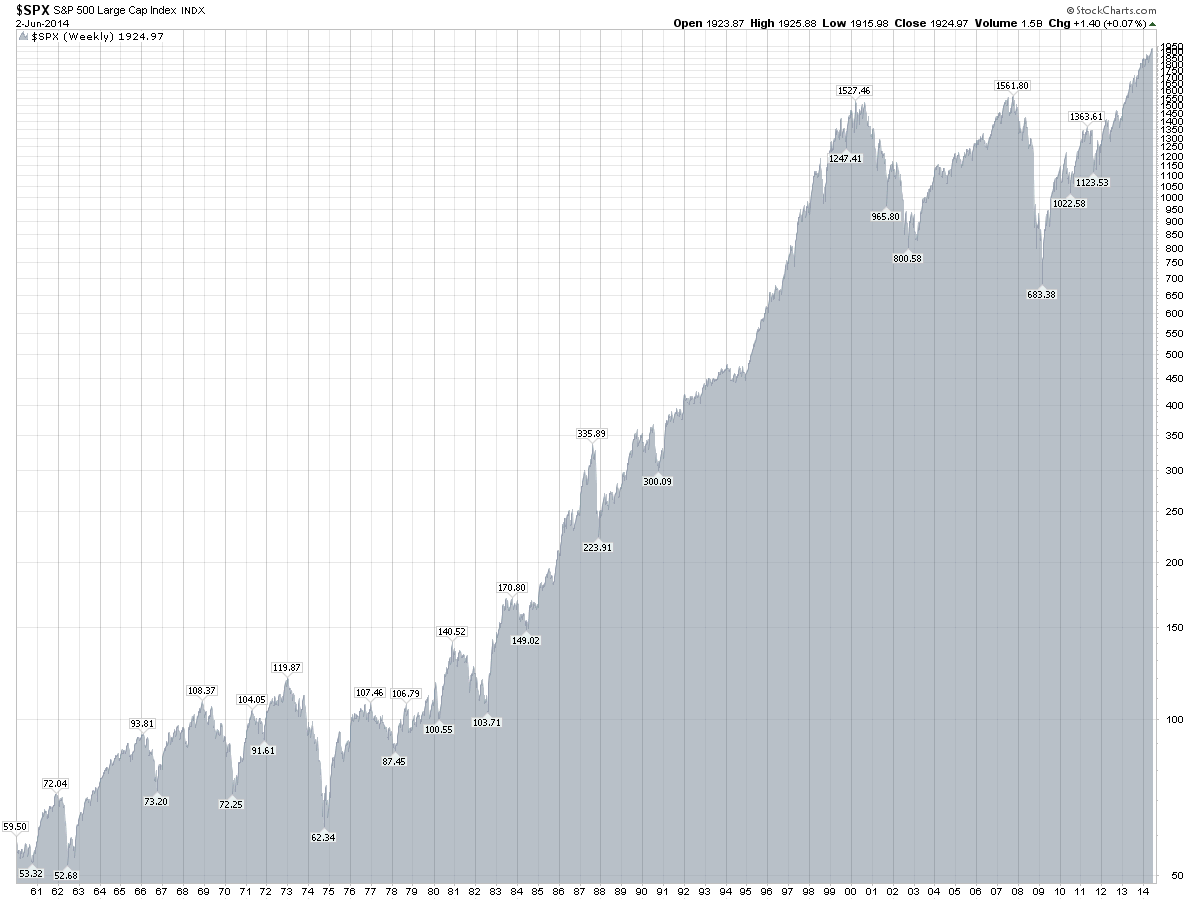

If one studies the “business cycle” over the last decades, one can see that it has a clear seven year period visible to the naked eye.

The below charts are of the S&P 500. Note the peaks in reverse order: 2007 and 2000 stand out, but the bond market crash of 94 and the crash of 87 are also on that same period. The downmarket period starting end of 1980 was adjusted quickly to support the Reagan Bush Administration’s lockstep with the goals of the transnational, transpersonal Empire, but the crashes of 1973 and 1966 appear to have been severe. We need to prepare for a year end crisis in 2014, with likely preview market adjustment (real world crises) downward at year end 2013 with sideways wobbling in distress throughout 2014.

The well reported effort of the “G20” (most recenly in James Rickards’ book Currency Wars) to impose a global currency (public SDRs) by 2018 will likely be accompanied by severe screw tightening to extract national and popular sovereignty concessions. See the article on the rise of the “Phoenix” in 2018 from the Economist of January 9th, 1988, reprinted below in full. The period 2014 -2018 and beyond is likely to be the most dangerous period in human history since the second world war.

As the reader will no doubt be aware, a broad concern regarding the current market period suggests that the tech and housing bubbles have been replaced by a government debt bubble. The mass foreclosure crisis of 2008 foreshadows a foreclosure crisis on national governments during the next phase of the cycle.

The attempt to foreclose on national governments globally is likely to be met with much fiercer resistance than the private property foreclosure crisis in America over the past five years. As the Central Bank continues its “quantitative easing” program to accumulate government debt and mortgages with ex nihilo “dollars,” its intent to control the monetary and real estate fate of the US becomes more and more apparent. Interestingly, it conceals its takeover of US real estate and sovereign power beneath an appearance of “stimulating the economy.”

I do not believe the Phoenix or the global government plan will be successfully implemented in the long run – nor will I support it – but I am concerned that any conflict that erupts domestically and internationally may be more severe than the Arab Spring and Occupy Wall Street response to 2008.

The Seven Year Business Cycle – Historical Notes

The seven year period of the business cycle is not an accident.

That there were seven years of bumper crop and then seven years of famine in the Bible story of Joseph and the Pharaoh may not have been a natural event divined in a dream by Joseph. The story more strongly correlates to the seven period interpretive cycles of the Bible: the allegorical creation days, the jubilee year cycle et al. It is built into the Kabbalistic numerological system:

https://judaism.about.com/library/3_askrabbi_o/bl_simmons_seven.htm

snip: “In the beginning… God created 7’s.

Oh sure, He created light and dark, the heavens and earth, too.

But for reasons unknown to us, He seemed to have a special

affinity for the number 7…”

This link describes the Kabbalistic number 7’s significance to contracts, treaties and bargains. There are plenty more references available if you google “kabbala number seven”.

This link describes the number 7’s significance among the Chaldeans of the same region and time period, and this link the number’s significance among the Egyptians.

What is more plausible to me is that the “famine” was a manipulation of the Egyptian agricultural system, using period standard methods described as “hydraulic dictatorship” in Karl Wittfogel’s seminal work on the subject, “Oriental Despotism.” Hydraulic dictatorship means rule by control of access to water, it was a standard feature of ancient empires. According to EconomicExpert.com, “Most of the first civilizations in history, such as Ancient Egypt, Mesopotamia, the Indus Valley civilization, China and pre-Columbian Mexico and Peru, were hydraulic empires.” These methods are similar to the way in which the business cycle is managed through increases and decreases in “liquidity” by the modern equivalent of the ancient rulers: central bankers (liquidity providers) and their political proteges.

The likelihood is that the famine was created not by God, but by some combination of Joseph, the Pharaoh and the priests (an archetypal instance of the relationship between financier, priest, and sovereign). Perhaps there was an original natural event or pattern in nature which eventually inspired the institutionalization of a management system to capitalize on it. Perhaps as now, even then there was intentional mismanagement of the economic (irrigation) system in order to produce certain power dynamics.

It is not so much fractional reserve banking that is fundamental to imperial global domination, but commodity control (food and water, land and livestock, precious metals). It is to this end that the fractional reserve banking enabled resource grabbing system is deployed, with the archetypal methodology described simply in Genesis 47, hidden in plain sight.

Read the familiar biblical passage again, as retold in David Martin’s insightful article on the subject:

https://www.invertedalchemy.com/2011/02/from-land-of-pharaohs.html

snip…

“47:13 But there was no food in all the land because the famine was very severe; the land of Egypt and the land of Canaan wasted away because of the famine. 47:14 Joseph collected all the money that could be found in the land of Egypt and in the land of Canaan as payment for the grain they were buying. Then Joseph brought the money into Pharaoh’s palace. 47:15 When the money from the lands of Egypt and Canaan was used up, all the Egyptians came to Joseph and said, “Give us food! Why should we die before your very eyes because our money has run out?”

47:16 Then Joseph said, “If your money is gone, bring your livestock, and I will give you food in exchange for your livestock.” 47:17 So they brought their livestock to Joseph, and Joseph gave them food in exchange for their horses, the livestock of their flocks and herds, and their donkeys. He got them through that year by giving them food in exchange for livestock…. ”

David’s point in the below paragraph will make audiences who are familiar with the importance of story (religion) in the construction of societal economic values sit up and take note.

“When a food commodity price shock hits – like the famine of old – the first response was to collect all of the money. Remember, at the time, this meant that there was a “rush to metals” not unlike our present day. One can readily see how the Pharaoh had gold sufficient to line tombs when you realize that, in the first year of famine, nationalization of gold assets was the first step to a new economy. This is the first record of a national reserve bank impulse in human literature.”

I wonder about the nature of the “reserve bank impulse.” Most standard justifications for the reserve bank impulse “scientifically” sever the loving and supportive relationship between God, Humans and Nature so evident in more balanced, indigenous and spiritual lifeways. As we can see in its most common implementations and contexts, the reserve bank impulse is primarily championed by dominating male God figures. It may also be described as a deception attempting to show by force, using self-fulfilling prophecy, that manipulating and controlling Nature (the Goddess) is superior to worshipping Mother Nature and integrating within Her.

David’s analysis is at times amusingly ironic: “At this point, I wonder how many of our religious right politicians take the time to realize that their Bible actually used nationalized socialism as a primary means of enacting “God’s plan”? ”

In addition, his article prompted a careful study of the below passage, which led to an important etymological insight into (trans)human nature through the lens of the Hebrew word for money: keceph:

The original passage is “Joseph gathered all the money that was found in the land of Egypt and in the land of Canaan for the grain which they bought, and Joseph brought the money into Pharaoh’s house.”

Click the word money above and you will get the original Hebrew word: keceph. Keceph means silver first, money second. It is very closely related to the word Kacaph (same three symbols), which means literally to become pale (like silver), and figuratively to long for, to desire or to be greedy. It is also closely linked to, and sometimes means shame, which can result in going pale, hence the figurative meaning. The complex ancient/modern assumptions and misunderstandings around greed, shame and desire are highlighted in these words, as is the relationship between silver and white skin.

Coming up next: an analysis of the number Seven in Ancient Egypt and Chaldea, the etymology of the word “seven” and the progression of “Judgment Day” hieroglyphs. Osiris sometimes holds just the crook and flail, and other times the crook, the flail and the scepter of Set. See if you can guess where the analysis takes us by reviewing the hieroglyphs themself at this website.

Please note that the coincidental use of the Greek word Phoenix (Benu in Egyptian) for the global currency described below is also not accidental, but summons a powerful symbol of the ancient world for the return or resurrection of a powerful being. Let us hope that the character of this being is defined more by its ancient symbolism signifying the height of the Sun’s power and the rise of the River of Life (the Nile begins to rise at the Summer Solstice) than its modern imperial incarnations.

“GET READY FOR A WORLD CURRENCY”

Get Ready for the Phoenix

Economist; 01/9/88, Vol. 306, pp 9-10

Jan. 09, 1988

“GET READY FOR A WORLD CURRENCY”

Get Ready for the Phoenix

Economist; 01/9/88, Vol. 306, pp 9-10

THIRTY years from now (written Jan. 9, 1988) Americans, Japanese, Europeans, and people in many other rich countries, and some relatively poor ones will probably be paying for their shopping with the same currency. Prices will be quoted not in dollars, yen or D-marks but in, let’s say, the phoenix. The phoenix will be favoured by companies and shoppers because it will be more convenient than today’s national currencies, which by then will seem a quaint cause of much disruption to economic life in the last twentieth century.

At the beginning of 1988 this appears an outlandish prediction. Proposals for eventual monetary union proliferated five and ten years ago, but they hardly envisaged the setbacks of 1987. The governments of the big economies tried to move an inch or two towards a more managed system of exchange rates – a logical preliminary, it might seem, to radical monetary reform. For lack of co-operation in their underlying economic policies they bungled it horribly, and provoked the rise in interest rates that brought on the stock market crash of October. These events have chastened exchange-rate reformers. The market crash taught them that the pretence of policy co-operation can be worse than nothing, and that until real co-operation is feasible (i.e., until governments surrender some economic sovereignty) further attempts to peg currencies will flounder.

But in spite of all the trouble governments have in reaching and (harder still) sticking to international agreements about macroeconomic policy, the conviction is growing that exchange rates cannot be left to themselves. Remember that the Louvre accord and its predecessor, the Plaza agreement of September 1985, were emergency measures to deal with a crisis of currency instability. Between 1983 and 1985 the dollar rose by 34% against the currencies of America’s trading partners; since then it has fallen by 42%. Such changes have skewed the pattern of international comparative advantage more drastically in four years than underlying economic forces might do in a whole generation.

In the past few days the world’s main central banks, fearing another dollar collapse, have again jointly intervened in the currency markets (see page 62). Market-loving ministers such as Britain’s Mr. Nigel Lawson have been converted to the cause of exchange-rate stability. Japanese officials take seriously the idea of EMS-like schemes for the main industrial economies. Regardless of the Louvre’s embarrassing failure, the conviction remains that something must be done about exchange rates.

Something will be, almost certainly in the course of 1988. And not long after the next currency agreement is signed it will go the same way as the last one. It will collapse. Governments are far from ready to subordinate their domestic objectives to the goal of international stability. Several bigger exchange-rate upsets, a few more stock market crashes and probably a slump or two will be needed before politicians are willing to face squarely up to that choice. This points to a muddled sequence of emergency followed by a patch-up followed by emergency, stretching out far beyond 2018 – except for two things. As time passes, the damage caused by currency instability is gradually going to mount; and the very tends that will make it mount are making the utopia of monetary union feasible.

The New World Economy

The biggest change in the world economy since the early 1970’s is that flows of money have replaced trade in goods as the force that drives exchange rates. As a result of the relentless integration of the world’s financial markets, differences in national economic policies can disturb interest rates (or expectations of future interest rates) only slightly, yet still call forth huge transfers of financial assets from one country to another. These transfers swamp the flow of trade revenues in their effect on the demand and supply for different currencies, and hence in their effect on exchange rates. As telecommunications technology continues to advance, these transactions will be cheaper and faster still. With uncoordinated economic policies, currencies can get only more volatile.

Alongside that trend is another – of ever-expanding opportunities for international trade. This too is the gift of advancing technology. Falling transport costs will make it easier for countries thousands of miles apart to compete in each others’ markets. The law of one price (that a good should cost the same everywhere, once prices are converted into a single currency) will increasingly assert itself. Politicians permitting, national economies will follow their financial markets – becoming ever more open to the outside world. This will apply to labour as much as to goods, partly thorough migration but also through technology’s ability to separate the worker form the point at which he delivers his labour. Indian computer operators will be processing New Yorkers’ paychecks.

In all these ways national economic boundaries are slowly dissolving. As the trend continues, the appeal of a currency union across at least the main industrial countries will seem irresistible to everybody except foreign-exchange traders and governments. In the phoenix zone, economic adjustment to shifts in relative prices would happen smoothly and automatically, rather as it does today between different regions within large economies (a brief on pages 74-75 explains how.) The absence of all currency risk would spur trade, investment and employment.

The phoenix zone would impose tight constraints on national governments. There would be no such thing, for instance, as a national monetary policy. The world phoenix supply would be fixed by a new central bank, descended perhaps from the IMF. The world inflation rate – and hence, within narrow margins, each national inflation rate- would be in its charge. Each country could use taxes and public spending to offset temporary falls in demand, but it would have to borrow rather than print money to finance its budget deficit. With no recourse to the inflation tax, governments and their creditors would be forced to judge their borrowing and lending plans more carefully than they do today. This means a big loss of economic sovereignty, but the trends that make the phoenix so appealing are taking that sovereignty away in any case. Even in a world of more-or-less floating exchange rates, individual governments have seen their policy independence checked by an unfriendly outside world.

As the next century approaches, the natural forces that are pushing the world towards economic integration will offer governments a broad choice. They can go with the flow, or they can build barricades. Preparing the way for the phoenix will mean fewer pretended agreements on policy and more real ones. It will mean allowing and then actively promoting the private-sector use of an international money alongside existing national monies. That would let people vote with their wallets for the eventual move to full currency union. The phoenix would probably start as a cocktail of national currencies, just as the Special Drawing Right is today. In time, though, its value against national currencies would cease to matter, because people would choose it for its convenience and the stability of its purchasing power.

The alternative – to preserve policymaking autonomy- would involve a new proliferation of truly draconian controls on trade and capital flows. This course offers governments a splendid time. They could manage exchange-rate movements, deploy monetary and fiscal policy without inhibition, and tackle the resulting bursts of inflation with prices and incomes polices. It is a growth-crippling prospect. Pencil in the phoenix for around 2018, and welcome it when it comes.