By Walter Borden

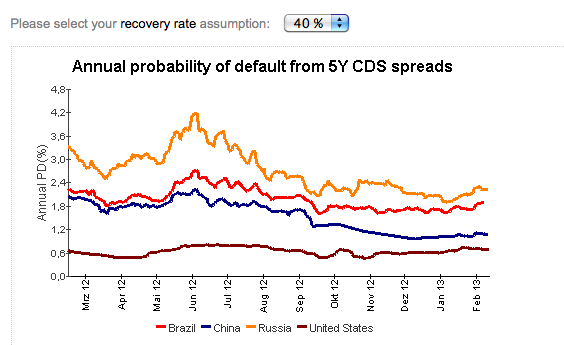

Have low interest rates formed an economic bubble? They are significantly lower than their 10 year average measured against similar conditions. Stephen Schwarzman of the Blackstone Group thinks so. He and others predict the next great fortunes will arise from precise timing of its bursting. Yet, fortunes and reputations have diminished over the past four years or so as a consequence of betting on its collapse ex ante. The markets continue to signal low, unchanging default risk for U.S. debt in both Credit Default Spreads (CDS) and the Exchange Traded Funds (ETFs) which short US debt. Economist and housing market expert Robert Schiller sees a cloudy outlook for mortgage rate increases. Paul Krugman, who correctly called the housing bubble in 2005, doesn’t see any evidence for a rate rise in the short and mid-runs.

Keynes famously said that in the long run we’re all dead. And, this is not only an Apres Moi, la Deluge argument. Time scales for ending our employment crisis matter to our children and grandchildren as well. History shows that economic policy and social policy timescales are often not commensurate. In policy circles and television talking head broadcasts, conventional wisdom categorically assumes sans empirics, interest rate trajectories with a strong upward bias. Yet, this bias distracts us from the real problem: the national U.S. employment problem and the long term damage of which seriously threatens our economy, our infrastructure, and our children’s future. How to bend this curve downward?

Further, ample evidence shows that debt stabilization comes more surely from economic growth at ~4%. Unemployment will definitely come down, as will the federal debt, if we grow the economy by this 4% benchmark just as we did in the last four years of the Clinton Administration. For example, in 2000 the unemployment rate averaged 4% per month and the U.S. had a budget surplus.

Two caveats–first, a contemporary growth path must be a sustainable one focused on infrastructure investment, education investment, and clean energy. Growth need not require a trade-off between pollution and high carbon emissions. Much is made of the high growth in India and China and their resultant carbon emissions. Less oft mentioned is that both have nascent Cap and Trade programs to offset their rampant pollution of vital natural, economic resources. Financial deregulation, fossil fuel extraction subsidies, and privatization schemes — such as selling our roads to Australian speculators — need to be put on hold because we have no evidence that they create sustainable jobs. Secondly, health care costs are driving our deficit, and while the ACA, or Obamacare is already bringing healthcare inflation down, more needs to be done such as preventing rampant regulatory capture that leads to $28,000 per vial drugs to reworking Medicare Part D to allow US taxpayers to negotiate with drug makers on price just like the VA and Medicaid. An NIH study states:

Extension of existing price setting mechanisms to Medicare could save tens of billions of dollars if prices similar to those already achieved by other federal programs could be reached. Whether or not this is a political or economic possibility, the magnitude of these savings cannot be ignored.

Low unemployment and reasonable wage growth will signal the time for focusing on national debt.

Logic dictates that simply because two things can happen, their probabilities aren’t equal. And, key economic and social indicators signal little inflation and interest pressure on the horizon, even if low rates can lead to bubbles. So the government can borrow now at historically low interest rates and invest the money in an infrastructure for a clean economy with a low probability of inflating a bubble in the short to mid runs. This in one of the ways a government that controls the world’s reserve currency is significantly unlike a household budget.

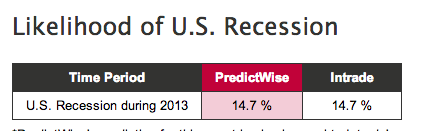

Many observers point to how Federal Reserve policies have kept interest rates low since 2008. However, the Federal Reserve announced during their December meeting that it will begin reversing its easing policies when the job market improves substantially, when the unemployment rate falls to 6.5%, or when inflation exceeds 2.5% per year. Current forecasts call for ~2% growth in the US in 2013 and ~15% chance of a recession — admittedly not an immaterial probability. So here again, 2013 likely will not vindicate interest rate speculators and bond short sellers.

In 1946 the debt was 120% of the GDP. It went straight down to about 32% in 1973. We had increased spending and deficits almost every year. The debt in dollars almost doubled. Real median household income surged 74% while CEO’s earned 50 times what their workers earned; it is 500 times today. The GDP averaged 3.8% growth. The U.S. resolved a debt crisis with more debt. Interest rates will rise eventually. That is not all bad. This would likely mean the unleashing of pent-up demand. And, the resultant weak dollar would boost exports of solar panels and the produce of sustainable agriculture for which there is strong demand in Europe and Japan. So, household books balance and run surpluses while the government takes on debt as the lender, consumer, and with QE, even borrower, of last resort.

Why is spurring demand and high employment more critical than deficit

reduction in 2013?

Most Baby Boomers will be hard pressed to fund retirement either by both having saved too little and suffered poor investment advice, or perhaps simply needing to draw down funds in a prolonged down market. A cursory look at the math gives us numbers that seem to fall into place like a game of Tetris. By 2030,

- Roughly 30% of the US population will be over the age of 65.

- According to MSN Money, about a third of those who are 10 years away from their planned retirement age have saved less than $25,000 which is $875,000 short of the Employee Benefit Research Institute suggested $900,000 that a typical person would need to live out his or her retirement years.

- Currently about 10% of seniors live in poverty; this number is bound to increase as more people who have inadequate savings reach retirement age, and Social Security fails to keep up with inflation.

Taking these numbers into consideration with the fact the consistent austerian policies very likely mean the U.S. faces a multi-decadal drop in aggregate demand — the main driver of growth which is in turn the most tried and true process for debt reduction — serious policy challenges face the US. This underscores the need to create jobs first and build a strong revenue base around a clean economy so that pollution does not eat away the gains via increased healthcare costs and decreased land values. Austerity mostly leads to more lay-offs, comparatively weak job creation (with low wages and benefit packages requiring taxpayers to pick up the costs, and a environment where wages stagnate or fall. Stunted wage growth may bode in the short run for the Oligarchy, but not the well being of the the majority of U.S. citizens whose labor and tax-dollars are used to finance its mighty military and Too-Big To-Fail-or-Jail banks.

After half a decade of stagnation, we are now looking at scenarios roughly 15 years out where senior discounts won’t suffice to get people into restaurants on Tuesdays, fill theater seats for matinees, and so on. A future, Speaker Boehner’s base will find their incomes dropping and wonder what is happening. Will they get wise and see that when people receive Social Security payments, they spend then in the local economy creating income for their neighbors? All the while highly affluent will continue their practice of waiting for the next bubble and/or offshoring their money to hedge funds and tax shelters.

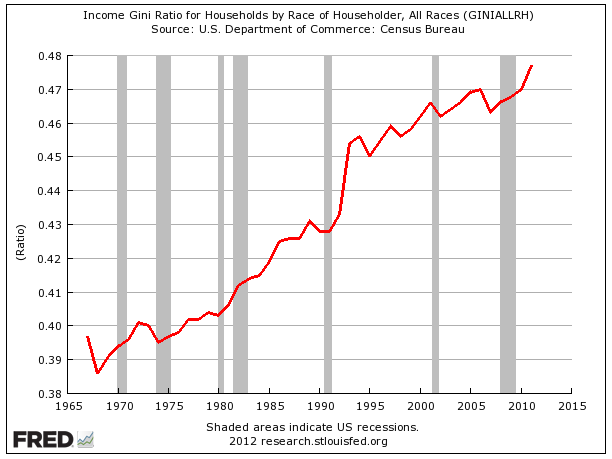

So in the end, the real job creators are the customers, and yet far too many politicians are willing to decimate the customer count, sitting idly by while income inequlity worsens. Without demand growth, it’s difficult to see market returns making up shortfalls much less adding very many new entrants via 401k’s investments. Another strong variable is competition for resources from Asia and Africa. Africa for instance is forecast to add 20 cities of over 10 million people in a decade or so. And, then there is inequality. To the right is a look at the Gini Coefficient (which measures societal income inequality–higher = more unequal) for the U.S. How can a healthy US economy when so many have so little with diminishing prospects to improve their share of US capital formation.

In short then, where will demand come from in the middle of this century? What policies can generate capital and social structures that can provide peace and security? It is generally agreed that extreme inequality is problematic for societies seeking these goals. This is why a progressive tax code is needed.

While it’s wise and natural to distrust government bureaucrats, recent history doesn’t say much for the corporate variety, either. Does anyone truly trust Wall Street with all their retirement? What if one has a job that is too demanding to become an expert investor and can not afford one to seek expert advice? Wall Street firms aren’t know for giving much attention to smaller clients. And pension funds are beinf quietly underfunded all across the US. It’s clear that Social Security Insurance is a far better steward for of baseline public financial security for the elderly and infirm.

Enter Impact Investing

Impact investing was pioneered by the Rockefeller Foundation as a complement to “social enterprise.” It was popularized by Antony Bugg-Levine, Amit Bouri, and the Global Impact Investing Network (GIIN) and is exemplified by the Acumen fund among others. Impact investing expands the application of capitalist ideas and methods to drive profit making that comports with the priorities of civil society. This can be contrasted with a future of an Ayn Rand dystopia of purely selfish corporations, much like 21st century Russia, rendered at tragic scale and great price to our economies and ecologies.

Regarding public life or responsibility to others, Ayn Rand wrote, “There is no such thing as the public, since the public is merely a number of individuals.” Does a long term period of slack demand portend an exposure of Austrian School naiveté or Chicago School laissez-faire dogma at long last? Can austerity matched with rising income inequality to provide solutions and to US unemployment and income/productivity inequalities? Not likely. And, there is little evidence that tax increases will do it either. We are unlikely to fully close the deficit via lower spending or the tax code. Deficits are closed via more growth. These other approaches do not work. Worse, Austrian austerian methods prove largely counterproductive time and again.

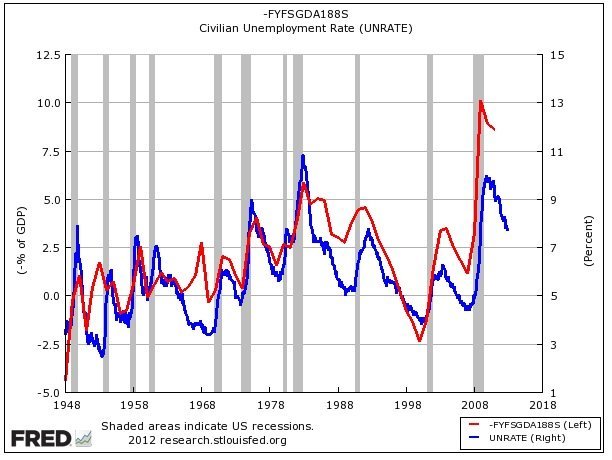

As this chart to right shows, an accurate predictor of deficits, going back decades, is the unemployment rate.

After all, it’s hard to start new businesses if no one can afford to purchase new products. In this environment, as the last 5 years has shown, the charity wheel alone is a necessary, but insufficient mechanism for peace, security, and shared prosperity. Can land and resource rents and robots save the day? Is an era of lowering and stagnating wages discreetly sought by some rentiers and plutocrats due to its building even greater leverage over labor and natural resources? It certainly consolidates their grip on the bulk of U.S. tax dollars and makes other public trusts and lands easier targets whether its public mineral rights or the likely gone but not forgotten ambition to privatize social security.

Janet Yellen, the vice chairwoman of the Federal Reserve recently found that a primary reason for the torpor of the US recovery is that government spending has been far more anemic in this business cycle than in the past. It’s a well established fact that big box store employees disproportionately must resort to Medicaid. Its expansion under the ACA has been shown to substantially increase revenues — even with the new costs factored in — for the states and thus improve their economies. Yet most oligarchs, their lobbyists, and a group of mostly Red States resist and refuse to embrace the expansion of Medicaid. Why? A look into the dynamics of Healthcare inflation is the subject of the next set of posts.