Does it make sense to tell someone that doesn’t have health insurance to go to the doctor? Does it make sense to expect jobless and underemployed citizens to save more? Many of the most profitable corporations across the US perennially underfund their pensions while simultaneously funding campaigns for privatization of social security paired with cuts to the program.

Pension shortfalls. Click to enlarge.

Yet, these same corporations oppose raising the cap on payroll taxes or asking Wall Street financiers to sacrifice via minimal financial transaction taxes common in the US during many a bull market and still common in the EU and Asia. All of this set against a backdrop of historically high corporate profits, S&P record highs, and stratospheric ratios of CEO pay to that of middle management and wage earners. The term generational theft is popular argot for corporate bureaucrats and their funding recipients in Washington, DC. Many of the CEO’s and hedge fund managers recommend pain of the majority and none for themselves. Yet, US taxpayers currently fund corporations at an historical scale via low interest rate loans and subsidies. This is the real generational theft: draining the the US middle class so financial speculators can ship away jobs, keep cash in tax havens, and speculate on Asian markets.

Gillian Tett writing in the Financial Times makes notes of a statement by a top executive of a consumer goods conglomerate:

We see a pronounced difference between how people are shopping today and before the recession,” the executive explained. “Consumers are living pay cheque by pay cheque, and they tend to spend accordingly. Then you have 50 million people on food stamps and that has cycles too. So for our business it has become critical to understand the cycle –when pay [and benefit] cheques are arriving.

Hence, the mostly austerity driven so-called recovery further reveals another deteriorating economic indicator for the middle class. Compare and contrast this with austerity champion the Walton Family and its Walmart. Without accounting for its massive local and federal tax breaks and subsidies, Walmart receives even more welfare from US taxpayers by paying its workers so little that they cannot afford healthcare and so must utilize social programs funded by their neighbors and fellow Walmart customers. In short, the world’s largest employer, after the US Department of Defense and the Chinese Military, relies on taxpayers rather than participation in the general welfare of the communities in which it operates and generates huge profits for its small group of majority shareholders (5% of of its owners possess 50% of its shares). Is this an example of good corporate citizenship?

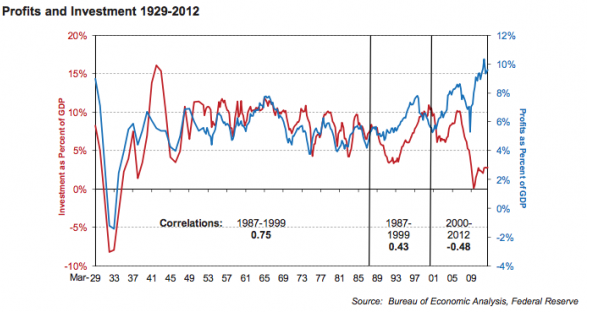

US Profits and Investment 1929 — 2012. Click to Enlarge.

Nevertheless, the most economically secure in our society mostly talk of deficits and are enabled by our nation’s highly consolidated media to dominate the public debate thereby granting them disproportionate exposure. Yet, their arguments that austerity and fiscal contraction will resolve the unemployment crisis fail logical and evidentiary tests time and again. Sequestration is projected to shave a point off GDP this year. As GDP shrinks consumers have less money to spend and consequently labor demands falls. Further, low-paying and low-to-no benefit jobs, which are the bulk of jobs now being created in the US, threaten a generation’s retirement security and access healthcare (health services as opposed to health insurance need disintermediation). Furthermore, corporations and the super affluent pay lower taxes than ever. Supporters for this program argue that it frees up capital to be reinvested in the economy. But, this not the pattern of the past 30 years. In the last decade the pace of reinvesting these perquisites into the economy or funding pensions has all but completely lapsed. Rather, these windfalls are shipped to hedge funds and tax havens. Additional study finds deeper problems.

That was my goal in my first law review article, “Improving Retirement Options for Employees”, which recently came out in the University of Pennsylvania Journal of Business Law. The general problem is one I’ve touched on several times: many Americans are woefully underprepared for retirement, in part because of a deeply flawed “system” of employment-based retirement plans that shifts risk onto individuals and brings out the worse of everyone’s behavioral irrationalities. The specific problem I address in the article is the fact that most defined-contribution retirement plans (of which the 401(k) is the most prominent example) are stocked with expensive, actively managed mutual funds that, depending on your viewpoint, either (a) logically cannot beat the market on an expected, risk-adjusted basis or (b) overwhelmingly fail to beat the market on a risk-adjusted basis.

Could this meltdown have been avoided? Should rating agencies have spotted it? Well, this is how it would work with the rating agencies when we were building a new CDO. They would tell us their parameters and criteria; if you meet this requirement, you get that rating and so on. And they gave out a free model so we could test our product and tweak our portfolio for the CDO until it fit, I mean get the rating that we wanted. We would do a lot of stress-testing ourselves too, of course we would. We’d pretend the market changed and run the models to see how our products would hold.

But what happened during the financial crisis was like a perfect storm. In our tests we would assume the market moved, say, 10% – while in reality it rarely moved more than 1%. Now the crisis happens and suddenly the market moves 30%. Our models were based on what we saw as normal. Now we saw numbers behave in ways barely conceived possible.

Consequentially, a quartet of corporate sector driven storm clouds hang on the horizon:

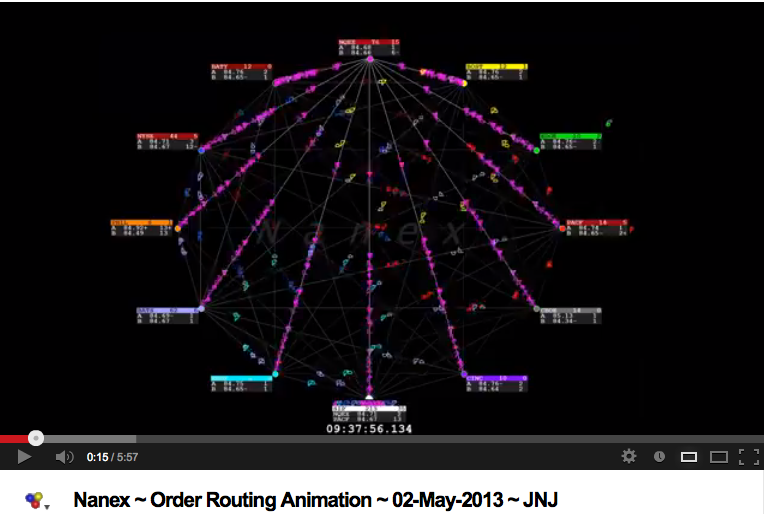

Nanex ~ Order Routing Animation ~ 02-May-2013 ~ JNJ .Click to Enlarge.

Underfunded pensions from corporations with record amounts of cash and an investment climate skewed towards insiders and Wall Street

Their ongoing failure to hire new employees and consistent blockage of publicly funded programs to fund infrastructure investment

A largely fossil fuel derived economy that requires large scale degradation of our present and next generations air and water resources

Over-priced/under-performing privatized healthcare drives healthcare inflation at unsustainable rates all the while forcing the good neighbors in US society to pick up the tab for the uninsured, many of whom are employed by highly profitable firms

Whats going on?

Why are record profits and CEO pay more and more divergent from the economic well being of the society’s whose labor and resources they use?

Asset Manager Jeremy Grantham (and lead of major Walmart institutional shareholder GMO) seems perplexed as well, offering the following observation:

There are times when the markets do not seem to be following the script properly, and we are left wondering whether we are dealing with a temporary anomaly or a more permanent problem. Today we are faced with one of these problems: the persistently high profit margins of U.S. corporations. High profit margins should not persist in a mean-reverting world, and yet profitability in the U.S. has been higher than long-term averages for most of the last 20 years, oddly pretty close to the same length of time that the U.S. market has been trading above replacement cost.

And he continues:

At first thought, it may not seem that odd that high profitability is associated with an expensive stock market – after all, shouldn’t investors be willing to pay more for assets that achieve a high return? But high valuations imply a low cost of equity capital, which should encourage corporations to issue more equity, and a high return on capital should encourage corporations to do more investing. These pressures should gradually push the cost of capital up and the return on capital down. But in the period since the mid-1990s, stock issuance has been down and corporate investment has fallen as well, in apparent contravention of the basic rules of capitalism. A high return on capital that occurred simultaneously with a high cost of capital – that is a market selling below replacement cost – would make sense because there is no discrepancy to arbitrage. The current situation is not supposed to happen, which makes it tricky for us to understand exactly when it will end.

US Profits vs. GDP. Click to Enlarge.

Add to this the increasing body of evidence that rate setting mechanisms for almost all forms of consumer debt and finance (the ~$500 Trillion pricing mechanism known as LIBOR) are subject to no substantive oversight and very often manipulated. This inevitably distorts the market, especially for retail investors and consumers. Matt Taibbi recently reported that commodity trading that impacts food prices (the ~$379 Trillion ISDAfix system) for Interest-Rate Swaps tool used by big cities, major corporations, and sovereign governments to manage their debt have been gamed by insiders for decades. Then, add in the ponderous functioning of ratings agencies paid by the very institutions and entities they are supposed to impartially rate, and we have chronic failures for our communities by significant portions of the global financial services sector. The scope of these failures include their ratings of pensions. Where, therefore, is the evidence that Wall Street is systemically capable of balancing its interests with those of Main Street? Is it not fair to ask if anyone really minds the conflict of interest, and its attendant risk at the upper echelons of Wall Street? How then can retail customers be competently served in the safeguarding of their retirements and savings by these institutions?

So, while the lack of transparency and efficiency of the financial markets for retail and non-professional, thinly capitalized investors offers little security, policy makers and think tanks funded by a great majority of Fortune 500 companies insist both on scaling back Social Security, forcing working citizens into demonstrably rigged financial systems and syndicates, all while neglecting their pension responsibilities.

One problem is that the major driver of growth and decline in profits — investment — has been decoupling from its traditional relationship since circa 2000, and worse yet since 2000, investment has fallen off to levels at their lowest since the Great Depression. Yet, as noted above, profitability has risen to a historic levels and ratios. Why exactly then, are corporations investing less than at any point since the Great Depression?

Ben Inker suggests that the issue can’t be with the profitability equation, which holds true because it is an “economic identity” derived from the Kalecki equation. He contends that this analytical framework suggests corporations treat their current profitability as a windfall rather than a permanent condition. This analysis fails to account for record size borrowing by highly profitable firms like Apple, which while it has ~$134 billion in cash overseas, would rather borrow money at historically low interest rates rather than pay taxes to its partners in American civilization, the US taxpayers. If they see such conditions as temporary, why borrow money they think they cannot repay? Is this an example of responsible corporate citizenship? If corporations are people, can this behavior be considered patriotic?

So, in effect they have record amounts of idle cash as do the other corporations taking advantage of these ultra low interest rates — US Airways, Morgan Stanley, Dish Network, JP Morgan, Verisign, Rosetta, Microsoft, and Walmart — yet they seek more all the while spurring precious little job growth in the US.

Some argue this state of affairs is because massive multinational corporations, based on predicted global demographics, are rather unconcerned about the decline of the American consumer. Over the next few decades, it is estimated that consumption by the US middle class will drop from around 25% to 5% of the global total while consumption by the Asian middle class will rise from around 10% to over 50% (these analyzes rarely account for the negative impact of rampant pollution on the cash economies like rice). As customers, US citizens, as the argument goes, are expendable in the long run.

Still others focus on changes in changes in productivity. As anthropologist David Graeber notes in an in a piece at the Baffler:

A renegotiated definition of productivity should make it easier to re-imagine the very nature of what work is, since, among other things, it will mean that technological development will be redirected less toward creating ever more consumer products and ever more disciplined labor, and more toward eliminating those forms of labor entirely.

Others point to increasing incentives to form cartels, virtual monopolies and monopsonies, and vested interests. This line of thinking notes how very well the rich have been doing over the past 30 years, even in terms of their share of labor income and hence the overall benefits of increased productivity. This rentier argument asserts that owners of the largest shares of capital are seeing their wealth concentrate and are incentivized to act like cartels. Some argue this is in itself a form of central planning (h/t Leland Lehrman).

Should not then, this increasingly permanent upper class, which not only fares far better in terms of labor income than the rest and in aggregation of GDP via persistently high dividends and stock buybacks, accumulate political opponents? It’s hard to gauge how political systems allowing for unlimited funding of politicians and elections might self-correct if these opponents cannot obtain similar amounts of funding for ever costlier campaigns.

Yet, if consequences do not materialize at the ballot box, at some point this capital hoarding has to evolve into spending if profits are to stay high, as there won’t be any purchasing power among the wage earners and the working poor. In this way, rising savings levels hurt corporate profits. Given that many of the wealthy generate income from government debt, part of the redistribution and purchasing power stimulation can come through government, in principle, but not if the government reaches a debt limit or is dissuaded from borrowing more because of phantom austerity pressures, that seem immune to steady, growing bodies of refutation from scholarly evidence, empiricism, and recent history.

Therefore, if the rest of households must stop dis-saving (despite stagnant wages and increased healthcare costs), this austerity requirement holds that the very affluent must dramatically increase spending to keep the system going. So far this has not happened, despite historically low tax burdens.

Izabella Kaminska asks in a post at Financial Times Alphaville if there are even enough goods and services for the rich to buy to make this work. She also posits, that even if it were possible, it would very likely almost increase the resentment of the the working poor until they took it out on them through the ballot box, if nothing else. The flaw in that argument is two fold: the post-Citizens United era in the U.S ( a good example here would be the Obama administrations embrace of COLA reductions and quiet but firm resistance to any sacrifice by Wall Street), and the lack of democracy in Russia and China, leaving only the EU and Japan as redoubts for democratic action to alleviate the stagnation and decreasing share of national incomes for the world’s largest economies’ middle class and working poor wage earners.

Kaminska goes on to note:

What Inker perhaps fails to recognize is that this may also be evolutionary game theory to some degree. There is now an interest in capital preservation, and the treatment of profits as a windfall, because capital itself is being compromised to some degree. More investment at this point may only lead to diminishing returns due to the general cornucopia referenced by Jeremy Grantham in his previous note. The incentive for rentiers to game the system — by holding back investment — is now greater than the incentive than to add services and output. Profits in dollar terms can only be guaranteed by contracting supply, not adding to it.

To get all evolutionarily stable strategy (ESS) theory on it, vested interests currently have a greater incentive than normal to effectively engage in price-fixing behaviour. And the usual processes that insure price-fixing pacts are unsuccessful due to treachery from within (lack of cartel discipline) are lacking because the treachery has evolved, potentially towards a more collaborative non-dollar defined benefit system.

Can these problems for the middle class and working poor be addressed within the framework of capitalism?

If the answer is only if we return to 1870’s or 1920’s unregulated, laissez-faire derived paradigms centered on Rand and Hayek, then likely no, not for the most of society and future generations. If the answer is rooted in a paradigm shift towards a philosophy of capitalism as a dynamic system which evolves and responds to feedbacks as surely as others, then, yes. Some examples that come to mind are Clean Economy infrastructure Investments, Elizabeth Warren’s effort to bring down interest rates on student loans, Public Banking Initiatives modeled on their highly successful instantiations in North Dakota, The Mondragon Corporation in Spain (which has quietly defied its slump), community based health care co-ops to name some specifics.

And in general Impact Investing by the top 100 Venture Capital firms are:

These Impact Companies (5 percent) were responsible for generating 10 percent of the overall revenue of the sample pool.

Over 6 years, their collective revenue grew by 146 percent, from $47 Million to $139 Million.

The impact companies also registered 21 percent higher revenue per employee than the non-impact companies.

And experience from the 1930’s shows public works projects and public-private partnerships, i.e. moving in the opposite direction of the austerians can put a generation back to work, generate revenue to pay debt, and provide security for our citizens in their elder years. After all, when GDP (the numerator) is growing faster than debt (the denominator) then public debt is shrinking. Now is the time for increased public investment in 21st century grade transport systems, as the American Society of Civil Engineers currently give the United States a D+ on the state of its infrastructure

Yet this is also not purely an argument assuming quick fixes from new regulations. Our policy makers are subject to a kind of cognitive capture, as are a great many of our regulators. President Obama choose Jack Lew and lead fund-raiser Penny Pritzker, two active participants in the sub-prime disaster, to key economic leadership roles in his administration. And it is well know that top management in banking and many other industries receive bonuses if they secure jobs in key US regulatory bodies and commissions. Which positions they depart in a few years time to return to lucrative roles in the private sector. So it’s fair to ask, whose interests are they serving? In many ways the regulatory system in the US has been hacked, to paraphrase Al Gore.

Another important example of regulatory capture are the inexplicable burdens on the US Postal System forcing it to prefund healthcare and retirement well out ahead of any norm even from the era of rational pension funding.

The above may help explain why regulations presented as remedies to subsidies for Too-Big-Too-Fail banks place undue burdens on community banks — the very banks whose primary activities are to finance the backbone of the American middle class — small businesses and entrepreneurs. For example, why no mandated lending to small businesses as opposed to a one-size fits all regulatory approaches? Cui bono? Such conflicts of interest present a systemic problem and thus a clear imperative to change the way regulations are made.

The US currently allows the mega-banks to borrow taxpayer money essentially for free then turn around and lend it to other huge companies for next-to-nothing, while letting the taxpayers foot the bill for keeping those interest rates low. We need more than Quantitative Easing (QE) and indeed even the Fed calls on Congress to do more in its latest announcement. To further compound the problems for working Americans, corporate boards benefiting from the US taxpayer largess have perfected tax avoidance schemes and simply borrow money instead of reinvesting their record profits in the US.

Bill Gross, the so-called Bond King of PIMCO, thinks there is no imminent bubble to burst in the bond market for a year or two (though he predicted such a burst 6 ago and PIMCO is increasing its purchase of US T-Bills, so it’s hard to know what such pronouncements really mean). Brad DeLong, on the other hand, astutely points to the hedge fund managers and their public dissent against QE and the Federal Reserve’s Ben Bernanke. That is to say, many financial wizards keep (wishfully) thinking of the Fed as if it were a rogue trader driving prices away from their natural value, like JP Morgan’s London Whale, rather than as a central bank working towards full employment and inflation rate targeting. Hence, their continued concerns (see most any post at ZeroHedge) at the failure of bond prices to crater the way they “should”. Further yet, it’s possible that the flood of liquidity is blowing a very different bubble in the financial sector as a whole. Stocks and bonds (both sovereign and private) are a shrinking portion of all financial assets. It seems that a comparatively small portion of QE liquidity sustains bond and shares values while a more substantial portion feed yet another hidden, unstable, expansion of hypothetical asset values such as derivatives, CDO’s, and other types of financial engineering, often trading in dark liquidity or dark liquidity a.k.a dark pools.

Preventing such a bubble in one asset class does not imply to stop cheap credit, but just to ensure that the extra money ends up in the pockets of families and not in the war chest of the latest quant fund. Here again, the Public Banking model constitutes robust options for reinvigorating the middle class with more targeted monetary policy.

In summary, in the opening decade and a half of the 21st century, a new superclass relentlessly tightens control on nearly all wealth in the US often choosing to send most of it overseas. Their share of such grows as real wages for the middle class remain generationally stagnant. The federal reserve aims to drive demand with large bond purchases that keep interest rates low. The quandary though is how can one drive demand without a mandate to invest in the U.S. or motivate such rentiers away from stock buybacks and increasing dividends? So while the Fed’s stated goal is to drive demand and bend the trend toward full employment, for now that money is mostly going to corporate balance sheets rather than outlays of capital and production.

Tax cuts are not helping either. In the current savings glut, much of any particular tax cut will go into savings, not because people expect higher taxes (they do not), but because they’re already on a course of saving (the poor save by paying off debt, the rich save by holding treasuries and cash). Unemployment for the wealthy is increasingly an abstraction and further disconnection from their neighbors comes from the myth that only 47% pay income taxes. Except they do. Over an average American citizen’s lifetime 86% will pay income taxes.

And so, we are stuck in a viscous cycle where an ever shrinking pool if owners of US wealth, assets, and resources obtain ever larger shares of them. Unsurprisingly, this does little to nothing to increase broad prosperity (despite the promises and assertions of Wall Street) as the wealthy simply channel this money into more investment accounts and offshore tax havens. Windfalls are not being re-invested by and large on goods or deployment of capital to productive use. What’s worse, the future security of the nation’s retirees as well as those entering the workforce is now neglected along with the very systems that allow commerce to flow — infrastructure. Add to this new technologies allowing increases in productivity while suppressing wages for the great many along with utter refusal to address climate change, a different and more salient threat of generational theft seems imminent. And it’s not that of the old taking from the young, as the fashionable argument goes, as shown above. The superclass has the resources to fully fund pensions and share in some pain in higher payroll taxes for the Social Security Trust without jeopardizing their competitiveness.

Heat Map of Chinese Pollution. Click to Enlarge.

Yet, the question is to what extent are these (ir)rational, however great, expectations, plausible? Voltaire wrote, “The comfort of the rich depends upon an abundant supply of the poor.” It need need not be thus and need be thus and the promise of the Enlightenment that such age old realities could be overcome in concert with a society where those that worked the hardest were proportionally rewarded while the bounty of such underwrote a social contract delivering baseline general welfare for all, including the impoverished and dispossessed. A century or so later, Hayek warned against “artificial demand”. Can endless financial speculation on hypergrowth in badly polluted regions like China — estimates of the percentage of its water that is undrinkable range from 40-70% — embody that very thing, posing as a miracle of capitalism? Building clean, sustainable infrastructure on a platform of plain vanilla banking in the US very likely is a cure to such danger, as the demand is real, high, and pent-up. And ultimately for those interested in the overall well-being of US civilization, full employment for now is surtout over inflation concerns,

In closing, Ms. Tett said it well in the Financial Times post cited above:

But, as the past five years have shown us, history does not go in a straight line, or proceed homogeneously. If you were to ask wealthy Americans to visualise the future, they might well describe it as a carefully calibrated road along which they expect to travel. But if you ask poorer Americans, who are scrambling from pay cheque to pay cheque, they are more likely to perceive the future as a chaotic series of short-term cycles. Economic polarisation, in other words, creates different cognitive maps, and also creates, of course, those subtle shifts in spending patterns that the big data experts in consumer goods companies now want to track.